UAH 5 billion scheme: Why tax authorities turn blind eye to bioethanol producers’ schemes

Bioethanol production in Ukraine is growing at a breakneck pace. Capacity already exceeds both export opportunities and legal domestic consumption. As a result, major market players are looking for ways to serve the needs of the illegal market.

According to preliminary estimates, the use of these schemes by just a few producers may have cost the state budget almost UAH 5 billion. And that is for just one year — 2025! For comparison, this is half the amount the authorities hope to additionally raise by introducing the controversial parcel tax, which will affect millions of Ukrainians. At the same time, this sum would make it possible to double the funding of the Ministry of Defense program aimed at scaling up middle-strikes, which are successfully destroying the logistics of the Russian occupiers.

If this sum is converted into the current issue of increasing payments to service members, UAH 5 billion would be enough to pay the updated monthly allowance of UAH 30,000 to 13,800 service members for a year. In other words, this is definitely a sum worth attention — and worth fighting for.

All the more so given that the existence of such schemes is no secret.

The Economic Security Bureau of Ukraine (ESBU) investigated several cases involving excise tax evasion in the production and sale of bioethanol and alcohol, but for various reasons they ended without results. At the same time, the production and sale of excisable goods should be controlled by the State Tax Service (STS), so any machinations in these markets are impossible without the "assistance" of its employees.

Business Censor looked into how tax evasion schemes work in the production of alcohol and bioethanol.

Alcohol and bioethanol: who may be exempt from paying excise tax?

Current legislation defines several main types of ethyl alcohol, apart from raw materials for the production of alcoholic beverages, in particular:

- undenatured ethyl alcohol — with an alcoholic strength by volume of 80% or more (UKTZED code 2207 10 00 90), as well as alcohol for medical purposes and the pharmaceutical industry (classified under code 220710 00 10);

- denatured ethyl alcohol — technical alcohol that contains denaturing additives, which makes it impossible to use it for the production of alcoholic beverages or in the medical industry (UKTZED code 2207 20 00 90);

- bioethanol — dehydrated ethyl alcohol (with a water content of up to 0.2%), intended for use as biofuel or a biocomponent (UKTZED code 2207 20 00 10).

According to the Tax Code of Ukraine, ethyl alcohol and bioethanol are excisable goods and are subject to excise tax at a rate of UAH 133.31 per liter.

At the same time, under certain conditions, a preferential rate of UAH 0 applies. This refers to cases where alcohol is used to produce medicines or vinegar, or where denatured alcohol is used to manufacture chemical and technical products, according to a list approved by the Cabinet of Ministers, or perfumery and cosmetic products.

To be entitled to apply the preferential rate, an alcohol producer must be included in the relevant Electronic Register maintained by the State Tax Service. It must also have the appropriate technological equipment, technical regulations, formulas, and so on.

A zero rate also applies to bioethanol that is used directly for the production of gasoline and other additives, or for the production of biofuel.

To prevent producers from being tempted to avoid paying excise tax without grounds, the State Tax Service must control the entire chain of production and supply of alcohol under the preferential "zero" rate. To this end, producers must equip excise warehouses on their premises with special meters, while an STS representative must be physically present at the production site itself.

At the same time, the law requires a separate license for the production of ethyl alcohol or bioethanol. This is logical, since the technological cycle for producing bioethanol differs significantly from the technology used to produce ethyl alcohol.

At the same time, enterprises that hold one of these licenses are allowed to produce other types of products (ethyl alcohol, denatured alcohol, or bioethanol), but only if they meet a number of conditions:

- the presence of a duly registered excise warehouse and a tax authority controller ("tax post");

- the availability of technical capacity for such production, which must undergo certification;

- entry into the STS Unified Register of information on obtaining permission to produce products different from those specified in the license.

This certainly does not sound very simple and is even somewhat confusing, but costly schemes are never simple. So, after working through the complicated details, operators found a "window of opportunity" for their fraudulent schemes.

How to avoid paying excise tax: what journalists and ESBU detectives found

The requirements set by the state for the production and sale of alcohol and bioethanol are among the strictest. And for good reason: excise tax revenues are among the most significant domestic sources of state budget revenue, which during the full-scale war are used to finance the Defense Forces.

But even during the war, some "entrepreneurs" are inventing new schemes to avoid paying taxes. Journalist Yevhen Plinskyi drew attention to one of them. According to his sources in the State Tax Service, a number of major bioethanol producers have found a way not to pay excise tax on their products to the state budget.

According to the journalist, this concerns Persha Podilska Enerhetychna Kompaniia LLC (PPEK), Zakhidna Etanolna Hrupa LLC (ZEH), and Bio PEK LLC.

These companies have licenses to produce bioethanol, but they have neither certified production capacity nor permission from the STS to produce denatured ethyl alcohol — the raw material for manufacturing excise-free "solvents."

In simplified terms, the scheme works as follows: instead of supplying bioethanol for fuel production, the enterprise "turns" it into "denatured ethyl alcohol" directly in the excise invoices. In practice, this allows the bioethanol produced to be used for making "solvents" without paying excise tax. These "solvents" already have a different UKTZED code (3814), and can be freely resold further without attracting unnecessary attention.

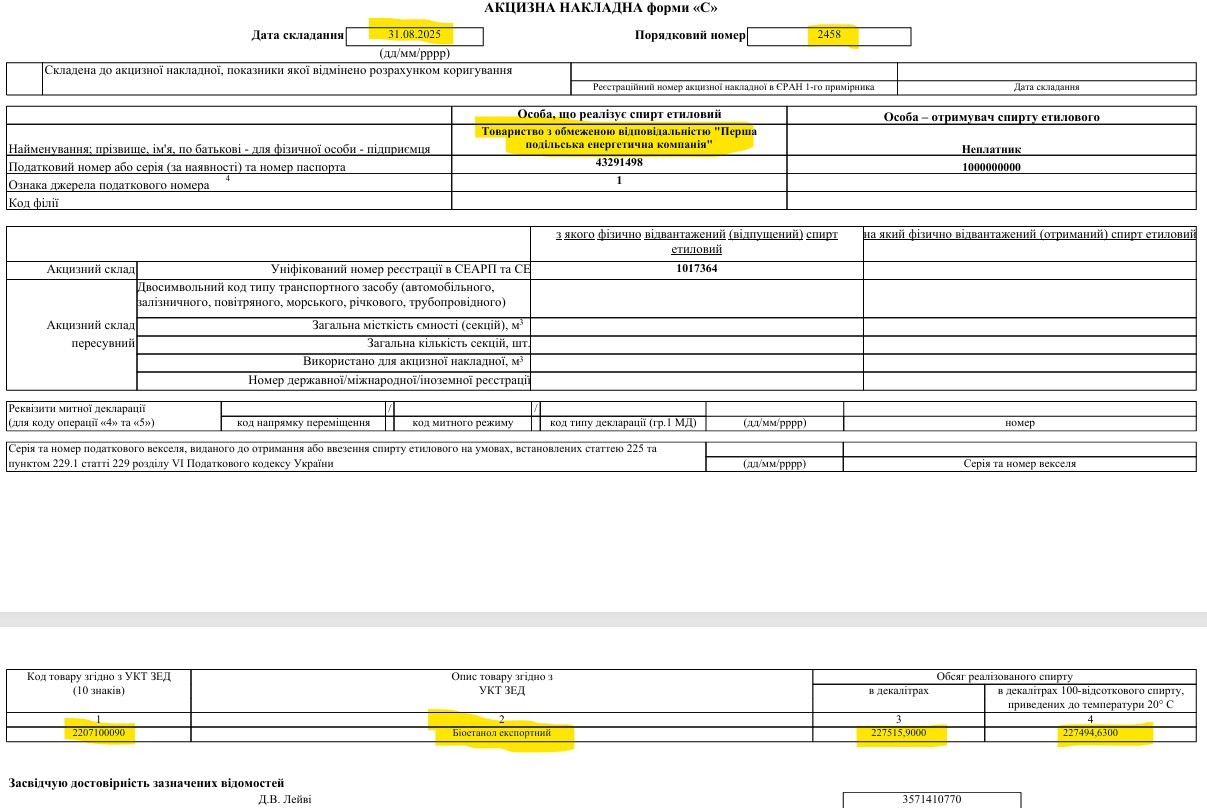

Plinskyi explains how this works using specific excise invoices as an example.

In particular, PPEK LLC and Bio PEK LLC directly indicate "bioethanol" in the product description, but instead of the relevant UKTZED code 2207 20 00 10, they specify another one — 2207 20 00 90 (denatured ethyl alcohol).

In effect, this allows bioethanol to be used for the production of "solvents" at a zero excise tax rate. However, the zero rate for bioethanol applies only if it is used for the production of legal fuel or for export.

In reality, the same bioethanol may be sold under the guise of "solvents" without payment of excise tax, with illegal mini-refineries among its main potential buyers, the journalist suggests.

This assumption is supported by several investigations by the Economic Security Bureau of Ukraine (ESBU).

According to the court register, back in November 2022, police officers in Lviv region stopped a tanker truck. According to the official documents, the tank was carrying Oksor U solvent produced by Persha Podilska Enerhetychna Kompaniia. However, the truck driver admitted that the tank actually contained gasoline. Moreover, the manager of the filling station to which the truck was headed was also present and confirmed that the tank indeed contained gasoline.

According to data from the YouControl system, Persha Podilska Enerhetychna Kompaniia LLC (PPEK) was registered in Lviv in October 2019. The company leases the bioethanol production facilities of the Teofipol Sugar Plant, with a capacity of 100,000 liters per day, and is Ukraine’s largest exporter of bioethanol, accounting for around a third of all exports.

Vadym Leivi is listed as the beneficiary of PPEK (with a 26.35% stake). He is a well-known entrepreneur from Khmelnytskyi, the owner of the Ukraina 2021 group of companies, and a former deputy of the Khmelnytskyi Regional Council from the Batkivshchyna All-Ukrainian Union party. He is also listed as director or co-owner of hundreds of companies, including Teofipol Sugar Plant PrJSC.

According to the investigation, PPEK officially sells bioethanol only for export, which allows it to apply the zero excise tax rate. At the same time, inside Ukraine, the company sells bioethanol to petrochemical enterprises, but under the guise of "solvents," so that it does not have to pay excise tax in this case either.

To substitute the commodity item, PPEK’s management ordered technical specifications for the production of "solvents." However, neither the company’s representatives nor the STS excise warehouse inspectors working on its premises were able to explain the differences between bioethanol and these "solvents" allegedly produced by the enterprise, or the mechanism by which bioethanol is converted into these chemical substances, according to the investigation data.

In addition, in October 2023, law enforcement officers conducted searches and seized documents confirming that PPEK had allegedly in fact produced "solvents" using equipment intended exclusively for biofuel production. However, in the summer of 2024, the then-unreformed ESBU closed the case.

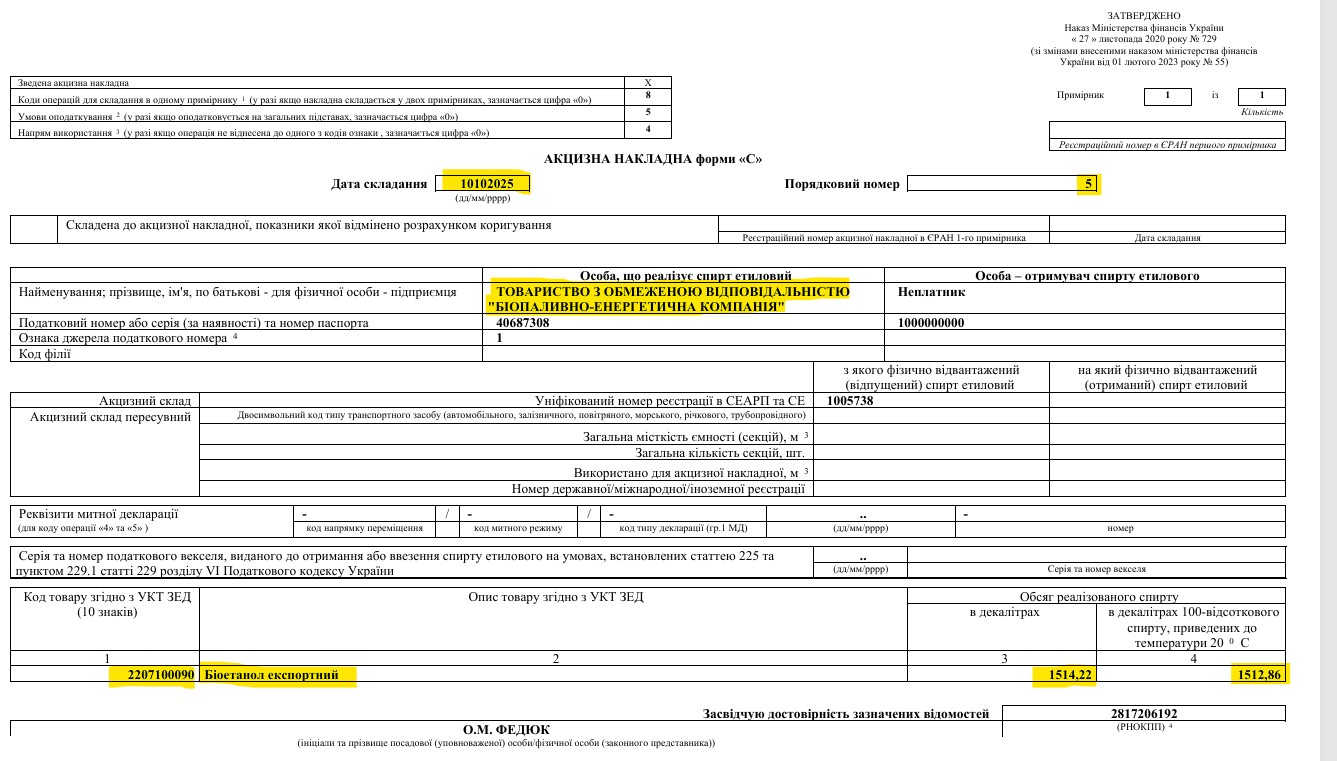

The ESBU managed to reach even more interesting conclusions in the criminal proceedings concerning Bio PEK LLC. According to the court register, the enterprise supplied "denatured ethyl alcohol" exclusively for export.

At the same time, the company sold bioethanol with the same physical and chemical indicators on the domestic market under the guise of BioNOL "solvent" with an alcohol content of 99.95%. To this end, technical specifications were ordered and developed in such a way that the physical and chemical indicators of the alcohol effectively did not change during the production of the "solvent." This essentially made it possible to illegally sell bioethanol without paying excise tax to fuel producers and filling stations, ESBU detectives suspected. By adding bioethanol to fuel, they thereby increased its volume and their own profits.

The detectives believed that the producer may have evaded payment of excise tax totaling UAH 324.61 million. In addition, investigators discovered unregistered bioethanol production facilities at the enterprise, where illegal products may have been manufactured.

According to data from the YouControl system, Bio PEK LLC was registered in the village of Rovantsi in Volyn region in 2016. Yevhenii Makara and Yaroslav Halkevych are listed as the company’s beneficiaries.

Moreover, a forensic examination of the seized samples, conducted on the instructions of ESBU detectives, established that BioNOL "solvent" matched bioethanol in its characteristics.

However, the court did not take the results of this examination into account, since ESBU detectives had allegedly improperly documented the "solvent" samples used for it. As a result, the director of Bio PEK LLC was acquitted in this case.

As for Zakhidna Etanolna Hrupa LLC, there are no criminal cases in the court register yet, which is not surprising, as this company is the youngest.

According to data from the YouControl system, Zakhidna Etanolna Hrupa LLC (ZEH) was registered in Khorostkiv, Ternopil region, in June 2023. Roman Vysochanskyi (50%) and Tigran Gevorkian are listed as the company’s beneficiaries.

Roman Vysochanskyi is also listed as the owner of the Khorostkiv Distillery and a number of other companies. His father, Volodymyr Vysochanskyi, is a long-standing business partner of businessman and former Svoboda party MP Ihor Kryvetskyi.

However, according to Plinskyi, law enforcement agencies have already taken an interest in this company as well. In particular, it has been established that ZEG, under the guise of bioethanol production, illegally produces ethyl alcohol, which is legalized through fictitious processing into Solventol "solvent" and sold on the shadow market.

Moreover, the company cannot legally produce ethyl alcohol, as it has neither the relevant license, nor certified technical facilities for its production, nor the relevant approval from the STS.

At the same time, according to the journalist’s sources in the tax service, this enterprise also manages to issue tax invoices specifically for ethyl alcohol, which would be impossible without the "assistance" of the tax officials themselves, who are supposed to directly control the entire process of production and sale of excisable products.

Why do tax officials "fail to see" the scheme?

The registration of invoices with the substituted UKTZED code should have been blocked by the tax service’s automated system — SEARP and SE (the electronic administration system for the sale of fuel and ethyl alcohol). But this does not happen.

The journalist’s sources in the alcohol market claim that there is a separate "tariff" for tax officials to "turn a blind eye" to this scheme. According to these data, it amounts to 10% of the revenue from the sale of the virtually produced "solvent."

For this enterprise alone, the total volume of risky transactions in 2025 and January-February 2026 amounts to 17.68 million liters, while estimated budget losses are assessed at over UAH 3.5 billion, Plinskyi notes.

According to calculations published by the journalist, in total, the three companies mentioned officially used almost 37 million liters of bioethanol and ethyl alcohol to produce "solvents" during 2025-January 2026, avoiding payment of excise tax. As a result, the state budget may have lost UAH 4.9 billion in revenue.

At the same time, the potential "benefit" for tax officials for "covering up" this scheme may have amounted to UAH 161.5 million, or more than UAH 12 million per month, the journalist suggests.

Where does "excise-free" bioethanol disappear?

Experts doubt that such a volume of alcohol-based "solvents" can be used in Ukraine for their intended purpose. Moreover, traditionally, the largest volumes of excise-free additives on the Ukrainian market have gone to illegal mini-refineries and filling stations for blending into fuel.

In addition, since May last year, Ukraine has introduced mandatory blending of 5% bioethanol into gasoline, and from July 2026 this share will increase to 7%. This should have increased demand for Ukrainian bioethanol, but currently there are almost no certified facilities in Ukraine for blending it with gasoline, and the vast majority of major fuel market players import the finished blend.

In practice, this means that Ukrainian bioethanol producers mostly export it to the EU, which allows them to apply the zero excise tax rate. However, export opportunities are limited: until recently, the quota for imports of bioethanol from Ukraine to the EU stood at 100,000 tonnes per year; last year, it was increased to 125,000 tonnes, and Ukrainian producers are already using almost all of this quota. At the same time, bioethanol production capacity currently amounts to 450,000 tonnes per year, and by the end of the year it may exceed 700,000 tonnes, according to the Ukrainian Association of Bioethanol Producers.

Therefore, bioethanol is often supplied to the domestic market under the guise of illegally produced "solvents." After all, there are almost no legal buyers of this raw material for blending with gasoline in Ukraine, which also allows producers to avoid paying excise tax. In addition, a separate license is required to produce fuel containing bioethanol.

At present, only one major filling station chain has its own facilities for blending fuel with bioethanol, but it produces it independently, says Serhii Kuiun, director of the A-95 consulting agency.

At the same time, he suggests that the bulk of excise-free bioethanol sold under the guise of "solvents" may end up at "grey" oil depots and filling stations, where it is illegally blended into fuel.

According to Serhii Kuiun, Ukraine’s shadow gasoline market is estimated at around 10%, or 200,000 tonnes per year. Therefore, the volume of "excise-free" solvents produced from bioethanol by just the three companies mentioned above (29,370 tonnes) is more than enough to cover the entire demand of illegal fuel operators.

However, the expert notes that such illegal gasoline containing bioethanol is usually produced without compliance with the proper technology, which may pose a risk to a car engine.

He notes that alcohol is hygroscopic, meaning it absorbs moisture both from tanks and from the air. If this process is not controlled, the fuel will eventually separate into water, alcohol, and high-octane gasoline, making engine operation impossible.

"Risks" or concern for "reputation": What do the tax authorities say?

After information about schemes involving duty-free bioethanol became public, Lesia Karnaukh, head of the State Tax Service, was forced to respond. She acknowledged that some companies are selling fuel at prices below the purchase cost, including delivery, and that this may indicate the use of illegal schemes involving the mixing of fuel with solvents.

"People are selling fuel for less than they pay for it. Cheaper than it costs to transport it. This is precisely one of the risks we are focusing on," she noted during the Petroleum Ukraine conference, which took place in early June in Warsaw.

According to Karnaukh, such actions could provide grounds for unscheduled and on-the-spot inspections of market participants.

However, the reaction to the possible existence of schemes involving the illegal production of ‘solvents’ from bioethanol without paying excise duty was radically different from that of the relevant department for the control of excise goods within the State Tax Service, headed by Khrystyna Bozhenko.

Business Censor approached the State Tax Service with enquiries to confirm or refute the information provided by journalist Yevhen Plinskyi. However, the tax authorities effectively refused to answer any of the questions relating to the activities of the companies mentioned in this article.

Moreover, in a reply signed by Khrystyna Bozenko, head of the relevant department at the State Tax Service, this refusal is explained as a concern for ‘protecting the reputation’ and ‘well-being’ of companies that may be involved in tax evasion amounting to billions, with the complicity of the tax authorities themselves.

It seems that for the first time in the history of our publication, in response to facts of tax manipulation uncovered by journalists, the State Tax Service has not merely issued a standard form letter, but has explicitly stated that our enquiries could harm the subject of our investigation. And this is despite the fact that the tax authorities showed no interest in the entirely reasonable assumptions that these companies’ activities are costing the state budget 5 billion hryvnias. We are publishing the full text of the responses provided to our editorial team.

Instead, the State Tax Service should not only have verified this information but could also have fined the companies—in the event that excise goods were used under a code other than that specified in the licence—at 200 per cent of the value of the goods, should the violations be confirmed.

Surprisingly, however, the tax authorities, at least publicly, do not even intend to respond to the scheme that has been brought to light, which provides further evidence to support the theory that certain tax officials are involved in its implementation. We are therefore now awaiting a response from the BES and the NABU. Corruption involving 5 billion hryvnias stolen from the army warrants attention at the highest level.